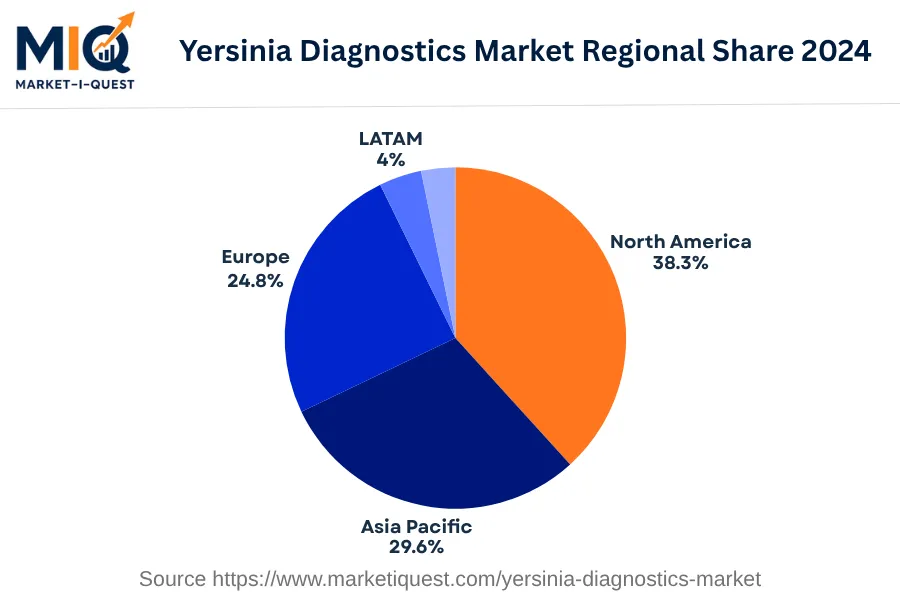

In 2024, the Asia Pacific Yersinia Diagnostics market experienced rapid growth as an urgent need for reliable diagnostic tools surged. Rising incidence rates of yersinia infections, particularly in densely populated regions like China and India, were major drivers. The increased government investment in healthcare infrastructure across Asia Pacific countries—including Japan, South Korea, and key ASEAN markets—enabled greater accessibility to diagnostic facilities, further boosting demand. Additionally, technological advancements in molecular diagnostics resulted in increased adoption due to improved precision and speed.

The year also witnessed shifting trends in buyer behavior, medical professionals across the region gravitating towards novel yersinia diagnostic methods, such as PCR and ELISA tests, over traditional culture-based tests. Aside from their enhanced sensitivity and specificity, top-notch reliability made these methods the preferred choice in hospitals, clinics, and diagnostic centers alike. Moreover, channel dynamics saw a significant shift towards digital solutions, with online portals becoming popular platforms for the procurement of diagnostic kits and tools. Strategic partnerships and acquisitions amongst major players in healthcare and biotech sectors served to streamline supply chains and expand product portfolios, amassing increased market shares. Moreover, stringent enforcement of diagnostic standards by government healthcare bodies like Australia's Therapeutic Goods Administration assured quality control, helping to maintain market integrity.