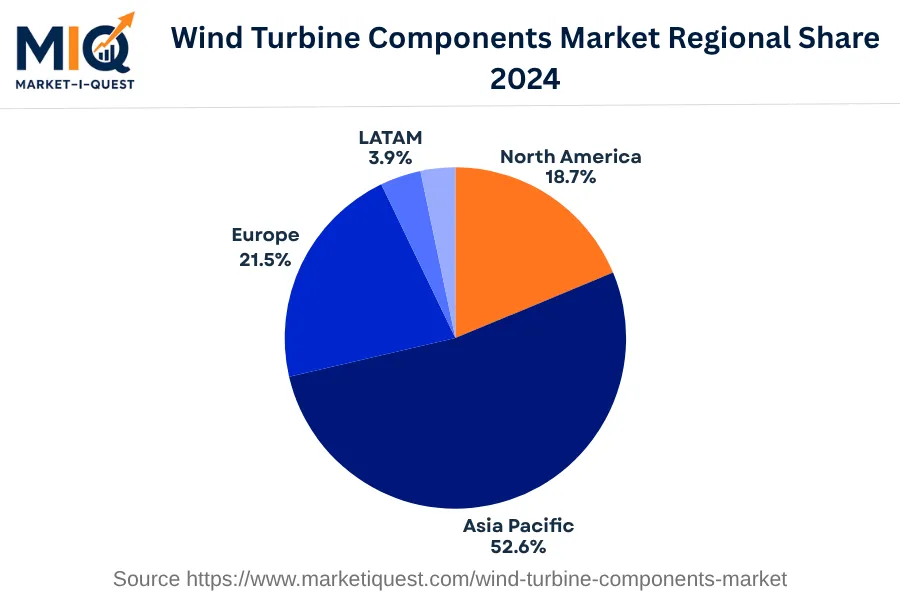

The Latin American wind turbine components market in 2024 was influenced by buoyant demand factors, legislative impulses, and competitive market dynamics. Enhanced investment in renewable energy infrastructure by Brazil, Mexico, and Argentina, accelerated by government incentives, powered an increase in demand for wind turbine components. Technological advancements in turbine design and materials, coupled with supply chain optimization, catered to the growing energy needs in the region. Key trends included an increased focus on cost-efficiency and sustainability. Both industry players and the end-users, predominantly utilities and large-scale manufacturing units, demanded high-efficiency, low-maintenance components. This led to increased application of advanced materials and smart operational technologies in component manufacturing.

Growing collaborations among regional and international manufacturers, as seen in Brazil and Mexico, instigated a healthy competitive environment and expanded the availability of technologically advanced products. Concurrently, the governments of Peru and Chile continued to enforce strict compliance with international environmental standards, encouraging green practices across the sector. The rise of digital platforms and e-commerce channels boosted direct customer engagement and widened market outreach in Colombia and Argentina. In sum, the LATAM wind turbine components sector in 2024 was characterized by increased demand, technological innovations, and strategic partnerships, all encouraged by supportive government policies and regulations.