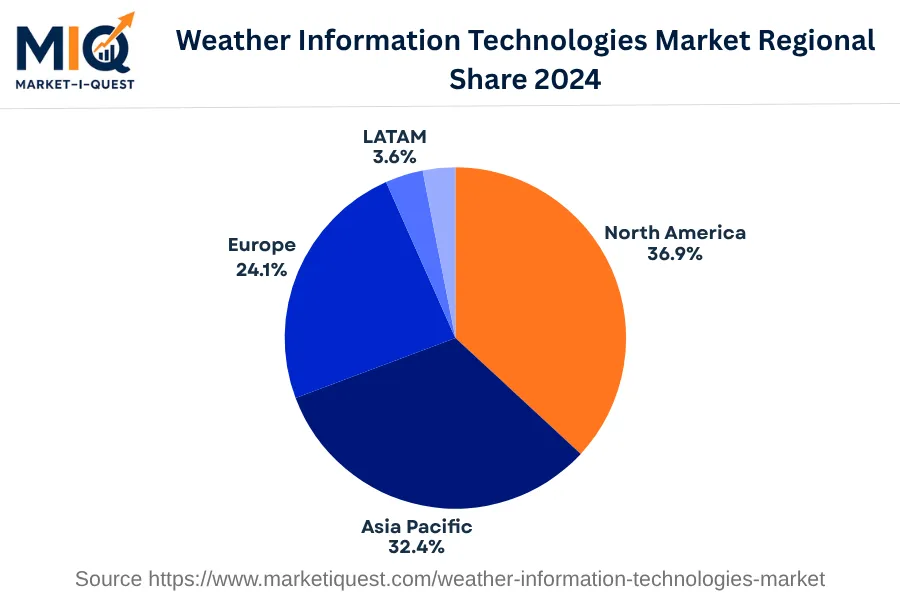

In 2024, North America's Weather Information Technologies Market experienced noteworthy growth primarily driven by varied market forces. Technological adoption rose as enterprises across the U.S., Canada, and Mexico leveraged weather data for operational efficiency. Regulatory standards emphasized accurate, timely weather forecasting, stoking greater demand for specialized technologies. Investments surged, with stakeholders exploring advanced solutions for predictive analytics.

Trends in the market included a shift toward AI and machine learning for data processing and meteorological predictions. Industries, namely utilities and retail, adopted these technologies to drive decision-making processes and manage supply-chain risks. The U.S. government demonstrated noticeable interest, integrating weather information technology into public safety protocols. These developments led to an increasingly competitive market landscape, driving innovation and partnerships.

Cloud-based platforms gained traction, underlining a shift in buyer behavior and channel dynamics. Standards in data security and privacy remained prominent, influencing technology design and offerings. Lastly, policy enforcement became a critical element, particularly in the U.S., contributing to market credibility and reliability. Altogether, North America's Weather Information Technologies Market saw a robust growth, reinforced by key drivers and trends. The confluence of technological adoption, investments, regulations, evolving customer behavior, and advanced products have shaped the market narrative of 2024.