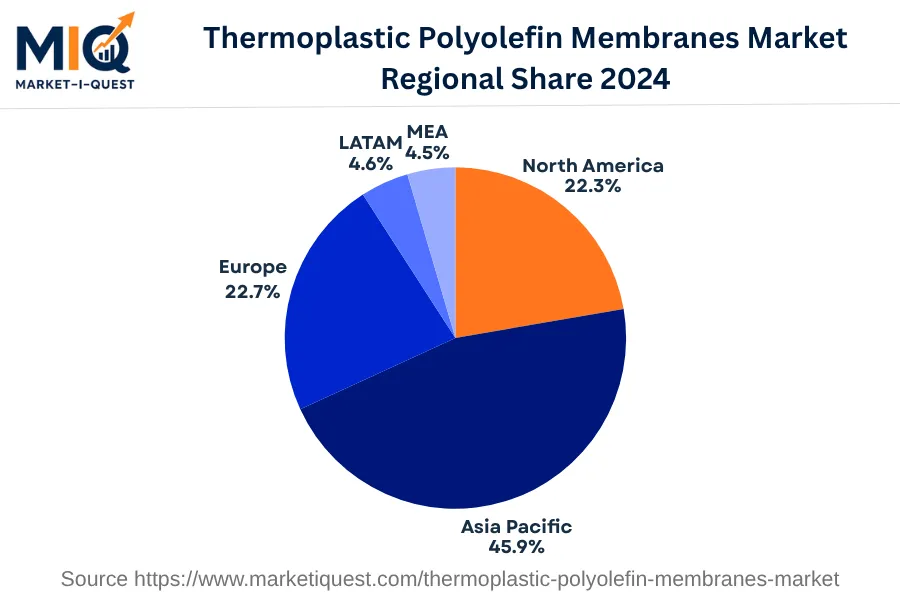

In 2024, Asia Pacific's Thermoplastic Polyolefin (TPO) Membranes Market saw remarkable momentum due to increased demand, technological adoption, and supportive policies. Demand was spurred due to rising ecological concerns and a steady growth in construction across economies like India, China and Japan. Chinese government’s push for greener construction practices and strong investment in infrastructure sector amplified the use of TPO membranes. Furthermore, South Korea's surging automotive sector projected a high demand for TPO membranes, fostering the market's sustainability. Integration of digital capabilities for product enhancement fueled technology adoption, notably in Australia and key ASEAN markets. Australia, for instance, implemented proprietary techniques enabling lighter, superior-quality TPO membranes.

Regarding trends, the pursuit for cost-effective and durable materials intensified competition leading to strategic mergers and acquisitions. Additionally, stricter regulatory compliance in China and South Korea influenced policy enforcement, promoting the usage of TPO membranes across sectors including enterprise, health, and utilities. Moreover, a sharp shift towards online sales channels influenced buyer behavior, with major manufacturers launching e-commerce platforms to facilitate sales, exemplifying the dynamic channel shift. Favorable policies, innovation, and environmental consciousness drove the TPO membranes market in Asia Pacific during 2024. Amid such development, it further positioned itself as an imperative component across various industry verticals.