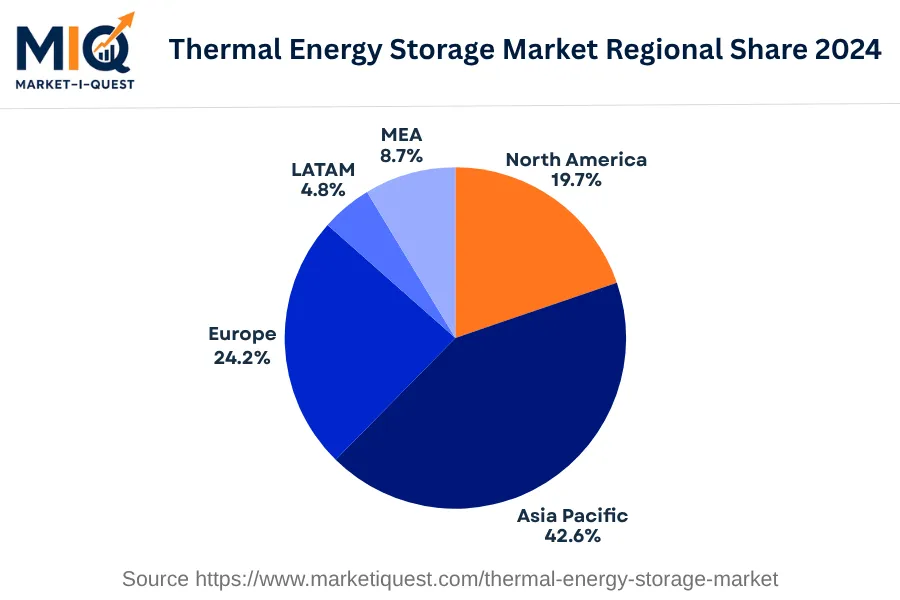

In 2024, the Asia Pacific Thermal Energy Storage market saw robust expansion due to multiple demand and supply triggers. Economic growth combined with industrial development, particularly in China, India, and Japan, facilitated increased energy demand, bolstering the uptake of thermal energy storage solutions. Regulations promoting renewable energy usage, as evidenced by China's Renewable Energy Law and India’s National Clean Air Programme, incentivized investments and adoption of advanced thermal storage technologies. Lastly, improving supply dynamics and competitive pricing augmented the market sentiment.

Shifts in consumer behavior towards energy-efficient solutions intensified, especially among enterprise and manufacturing sectors. Technological innovations in phase change materials and molten salt storage, primarily in Japan and South Korea, redefined product landscape. Channel dynamics leaned towards direct-to-consumer and e-commerce sales, especially in rapidly digitalizing markets like China and India. An increase in partnerships and mergers, such as between SunPower of Australia and Tomakomai of Japan, was noted, facilitating cross-border technology transfers. Stricter policy enforcement, such as the Renewable Energy Certificates in India, accelerated adoption, steering market trends.

This era in the thermal energy storage market was marked by a powerful interplay of demand factors, regulatory support, innovative technology adoption, and changing buyer behavior, particularly in China, India, Japan, South Korea, and Australia.