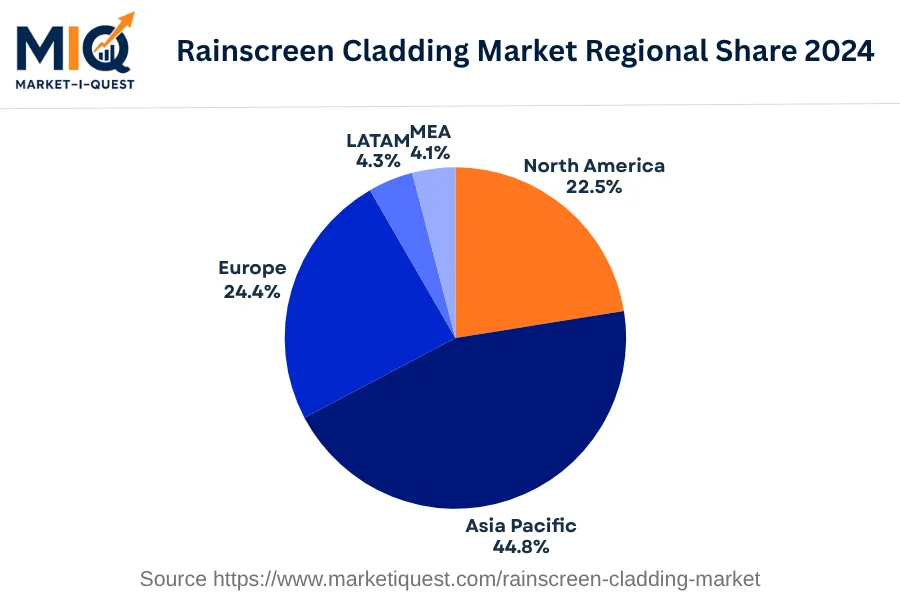

In 2024, the Rainscreen Cladding Market in the Middle East and Africa epitomized substantial dynamism. Heightened urbanization in Kenya, Nigeria, and Saudi Arabia, and stricter fire safety protocols, particularly in Israel and United Arab Emirates, stimulated demand for rainscreen cladding. Rapid investments in infrastructure, as in Qatar's Lusail City, also amplified uptake of this technology. Nevertheless, volatile raw material prices, specifically in Egypt and South Africa, imposed constraints on the supply chain. Shifting buyer preferences veered towards sustainable and energy-efficient buildings, underlining the trend of high-performance, eco-friendly rainscreen cladding systems within government, healthcare, and retail sectors. In the telecom and financial services industry, particularly in Kenya and Nigeria, maintenance-free and durability factors were the major procurement determinants. Technology advances prompted the expanded use of integrated rainscreen systems in new architectural frameworks mainly in UAE and Israel.

Policy enforcement in the region underscored adherence to ASTM E2273-03, a standard concerning rainscreen drainage efficiency, shaping manufacturing practices. Meanwhile, collaborations and M&A activities were observed especially in the oil and gas sector in Saudi Arabia and Qatar, indicating a strengthening of the sector's internal supply chain. Thus, market drivers and trends in 2024 exemplified an intricate interplay of demand factors, investment dynamics, technology, and regulatory adherence.