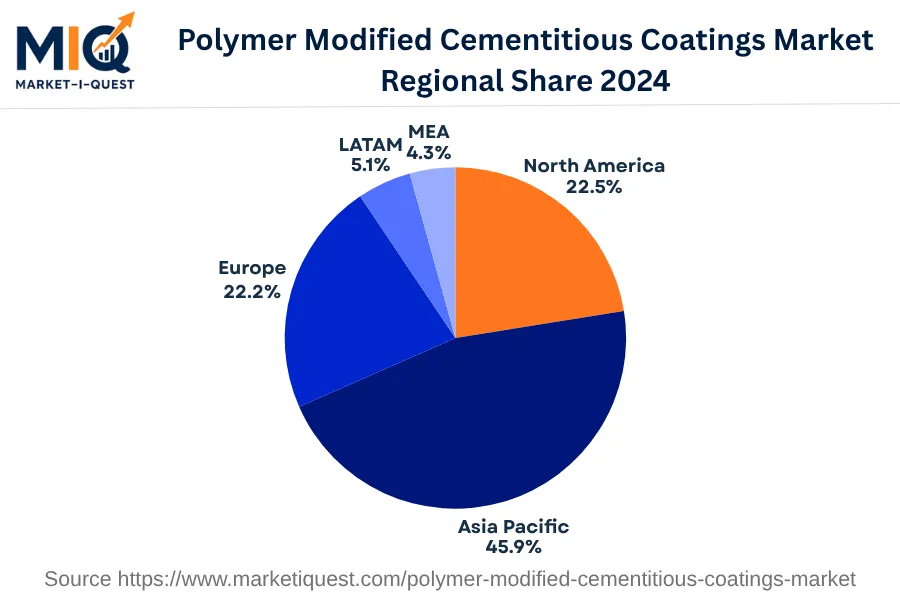

In 2024, the Polymer Modified Cementitious Coatings market in Middle East and Africa witnessed significant growth, particularly driven by increased investment and infrastructure development. The robustness of the oil and gas sector, particularly in countries such as Saudi Arabia, United Arab Emirates, and Qatar, created a need for more durable, efficient, and weather-resistant protective coatings for pipelines and industrial facilities. This, coupled with stricter government regulations in Nigeria and South Africa to ensure infrastructure longevity and sustainability, fueled the demand.

Simultaneously, widespread adoption of advanced coating technologies in industries such as telecommunications, manufacturing, and healthcare added momentum to market expansion. Specifically, the rise of mega-scale construction projects in Egypt and Israel led to incorporation of advanced materials, including Polymer Modified Cementitious Coatings.

In terms of trends, the push towards product innovation witnessed a surge, steered by buyer demand for versatile, high-quality products with longer lifespan. Mergers and acquisitions in the sector also shaped market dynamics, with focus on expanding portfolio and market reach. Finally, increasing enforcement of construction and environmental standards boosted demand for durable, high-standard coatings and moulded the sector direction in Kenya and other emerging markets. In general, the increased demand for Polymer Modified Cementitious Coatings in Middle East and Africa can be attributed to the region's dynamic infrastructure development, technological advancements, and tightening regulatory environment in the base year 2024.