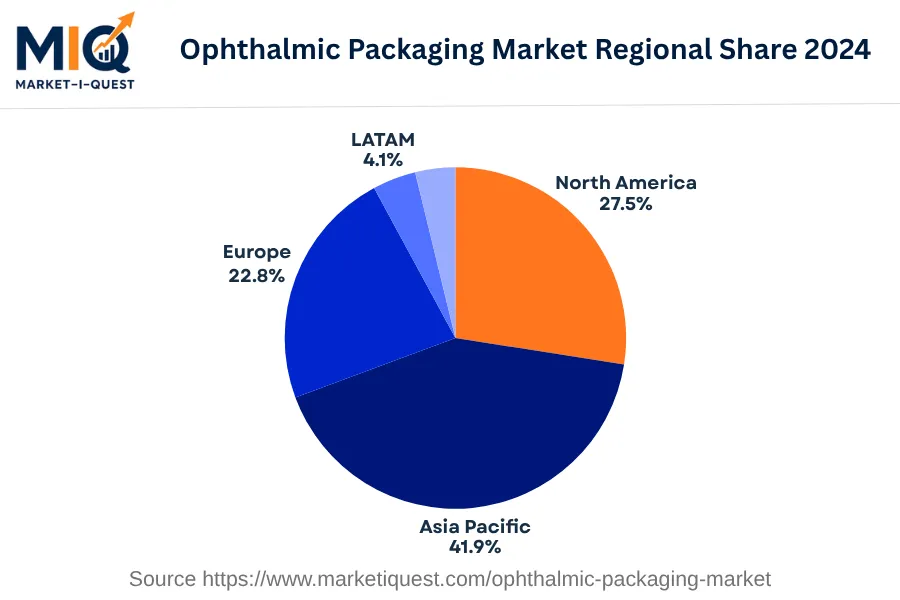

In 2024, the ophthalmic packaging market in Latin America witnessed significant activity, driven primarily by demand for advanced eye care products and influencer diseases like glaucoma and cataract. Increased investment in healthcare infrastructure across prominent LATAM nations including Brazil, Mexico, Argentina, Colombia, Chile, and Peru, backed by governmental regulations advocating quality packaging, fueled the market's growth. The wide adoption of technology in the packaging process also played a crucial role, enhancing efficiency and safety standards.

In terms of trends, changing consumer preferences toward innovative solutions characterized the period. There was a discernible shift towards more sustainable, eco-friendly packaging options, reflecting greater environmental consciousness among consumers. Digital channels emerged as vital platforms for distributing and marketing ophthalmic products, enhancing access and visibility. Significant strategic partnerships and M&A activities were observed, predominantly aimed at broadening product portfolios and strengthening market presence. Lastly, stricter policy enforcement around packaging norms governed much of the sector's activity in 2024. The market catered predominately to healthcare institutions, government-backed programs, and retail pharmacies. In particular, Argentina, with its advanced healthcare sector, and Brazil & Mexico, with their massive population base, stood out as significant consumers of ophthalmic packaging. Several manufacturing companies also emerged as key clients, relying on reliable packaging solutions to bolster their products' shelf life and appeal.