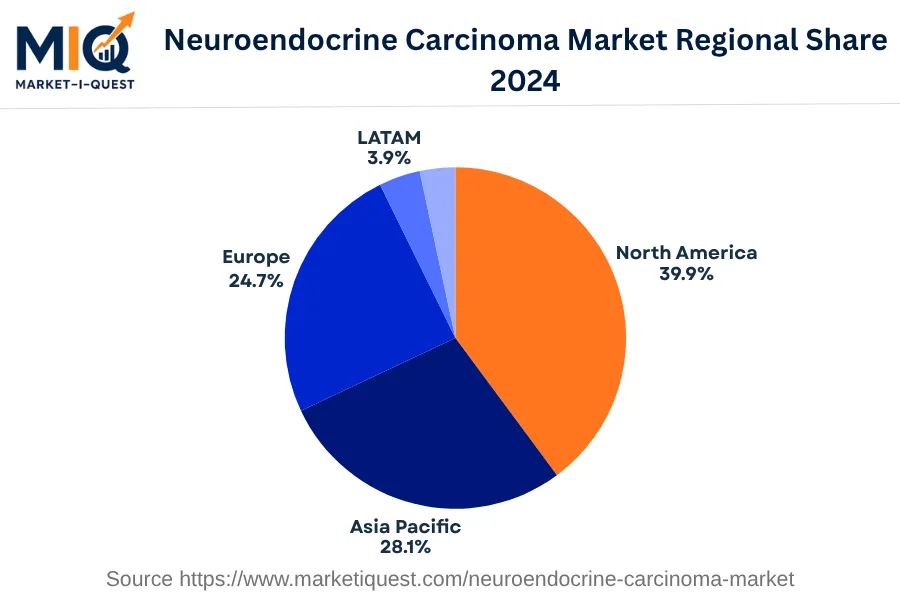

In 2024, the Neuroendocrine Carcinoma market experienced exponential growth across Asia Pacific, underpinned by incisive factors and emerging trends. An increasing demand was visible, mainly due to a steep rise in neuroendocrine carcinoma cases in populous nations like China and India, highlighting an improved diagnostic landscape. Additionally, Japan and South Korea's heavy investment in advanced healthcare infrastructure bolstered the market's acceleration. Technology adoption in Australia's healthcare sector also notable, with a significant number of medical centers incorporating technologically advanced disease screening methodologies, amplifying supply dynamics.

Key trends echoed market developments. A distinct buyer behavior was observed; despite the treatment's high cost, patients inclined towards advanced therapeutics, largely due to increasingly prevalent insurance coverages. Simultaneously, product shifts emerged, with an emphasis on immunotherapy, in sync with global health paradigms. In terms of channel dynamics, digital platforms, particularly telehealth, were successfully leveraged for patient consulting, diagnosis, and treatment recommendations in ASEAN markets. Sector-wise, government and healthcare remained prime contributors, specifically in China, where state-run healthcare entities facilitated widespread disease screening programs. Surprisingly, a surge in manufacturing entities specializing in the production of relevant medicaments was observed, implicitly supporting the market's development while rendering the retail sector conspicuously involved. Unprecedented partnerships and M&A activities occurred, such as those between leading pharmaceutical firms and clinical research organizations, underlining the market's robust nature in 2024.