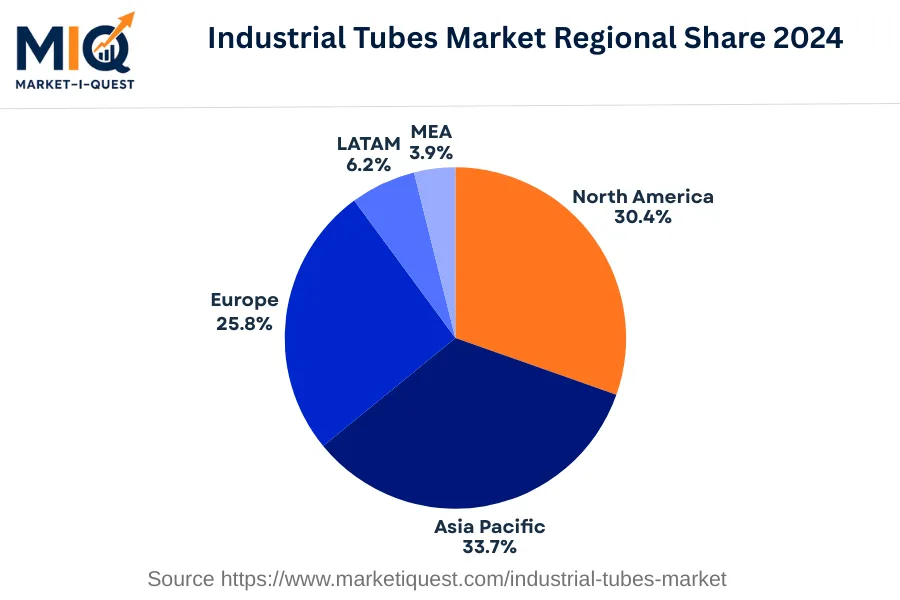

In 2024, the Industrial Tubes Market in the Middle East and Africa is characterized by robust demand driven by key sectors like oil, gas, manufacturing, and utilities. Factors like increased investments in infrastructure and energy projects, particularly in Saudi Arabia and the UAE, are leading to heightened demand for industrial tubes. Regulatory frameworks, like Saudi Arabia’s Vision 2030, promote local manufacturing, thereby influencing supply dynamics and encouraging technology adoption. Rising energy costs influence pricing strategies, impacting buyers’ procurement processes across various industries.

In 2024, the Industrial Tubes Market in the Middle East and Africa is characterized by robust need driven by key sectors such as oil and gas, manufacturing, and utilities. Factors like increased investments in infrastructure and energy projects, particularly in Saudi Arabia and the UAE, are leading to heightened requirement for industrial tubes. Regulatory frameworks, like Saudi Arabia’s Vision 2030, promote local manufacturing, thereby influencing supply dynamics and encouraging technology adoption. Rising energy costs influence pricing strategies, impacting buyers’ procurement processes across various industries.

Concurrently, the buyer behavior is shifting towards sourcing high-performance materials that enhance durability and efficiency. South Africa and Kenya are seeing an uptick in sustainable practices, prompting companies to seek eco-friendly tube solutions. The market is experiencing an integration trend through partnerships and mergers, enhancing supplier capacities and technological advancements. Furthermore, enforcement of standards, like the South African Bureau of Standards (SABS) regulations, is driving compliance in product quality and safety, affecting suppliers in the region. Overall, the market's direction in 2024 reflects a complex interplay of regulatory, economic, and technological factors impacting need and supply across key industries in the Middle East and Africa.