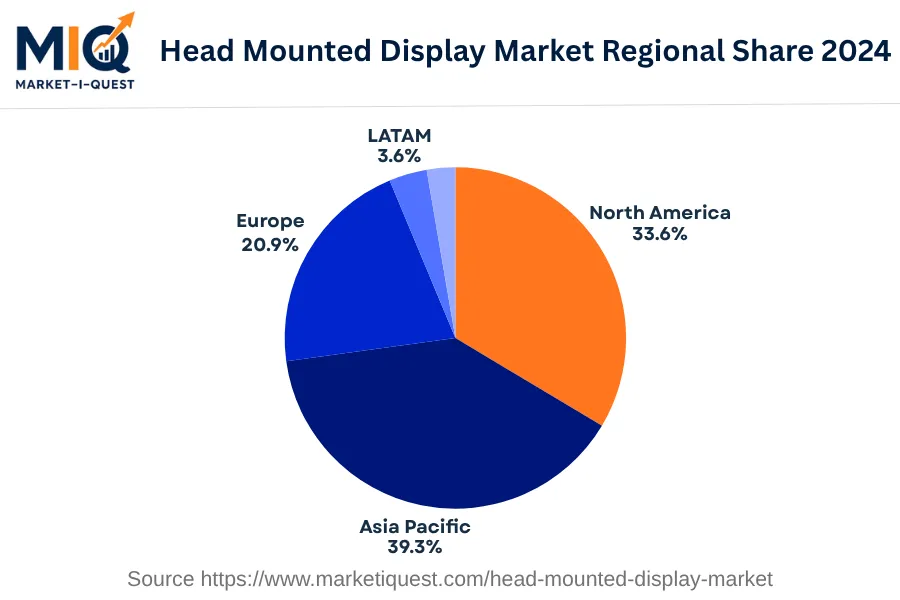

In 2024, the Head Mounted Display (HMD) market in the Asia Pacific witnessed dynamic competition and technology adoption. Multiple factors drove this vigorous market environment. Firstly, rapid technological advancements in virtual and augmented reality in countries like China, Japan, and South Korea fueled an increased demand for HMDs. Additionally, the relaxation of regulations in India, Australia, and key ASEAN markets stimulated substantial investment in the sector, opening up new jolts of unprecedented market growth. The availability of favorable manufacturing conditions across the aforementioned markets prompted manufacturers to intensify their operations, further propelling the supply dynamics.

Shifting trends played a crucial role in shaping the HMD market. For instance, consumers increasingly preferred wireless HMDs, prompting product realignment by major manufacturers. The online retail channels became preferred platforms for purchase, facilitating easy accessibility and broader choices for consumers. Sectors such as healthcare, manufacturing, and gaming saw increased uptake of HMDs, driven by specific industry demands. Policy enforcement by regional governments, particularly in China and Japan, dictated safety and quality standards for manufacturing and selling HMDs, altering the competitive landscape. Lastly, there was an uptick in strategic partnerships and M&As in the Asia Pacific to strengthen market presence, offering significant potential for innovative technology integration.