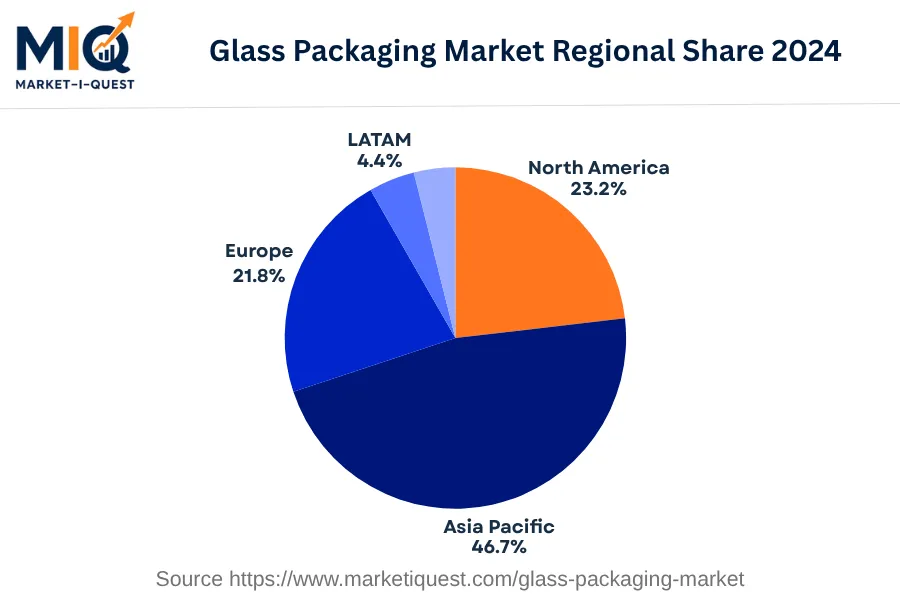

In 2024, the Glass Packaging market in Asia Pacific demonstrated significant growth, largely driven by increasing consumer preference for sustainable packaging solutions. China's stringent environmental regulations pushed manufacturers towards recyclable materials, enhancing demand for glass packaging across sectors such as beverage, pharmaceutical, and cosmetics. Similarly, India saw heavy investment from global giants like Verallia and Owens-Illinois in establishing advanced glass packaging facilities. Meanwhile in Australia, increased technology adoption in manufacturing plants promoted efficient production processes, further stabilizing market growth. Consumer trends exhibited a keen focus on glass packaging's advantages—transparency, high-grade aesthetic, and chemical inertness. Japan, among other countries, registered a high demand for glass packaged products in its vibrant retail sector due to changing consumer behavior favoring premium, quality-safe products.

A noteworthy shift was the increased use of lightweight glass in South Korea, given its potential to reduce transportation costs. Key ASEAN markets, particularly Thailand and Indonesia, highlighted a surge in partnerships and collaborations between enterprises and glass packaging manufacturers to meet growing consumer demands. Multiple sectors contributed to market enthusiasm, notably healthcare for its persistent need for secure, chemically-stable packaging solutions and retail for the higher aesthetic appeal glass presents to discerning consumers. Both sectors demonstrated how the broad adoption of glass packaging is resulting from the coalescence of numerous demand factors, regulations, and shifting preferences.