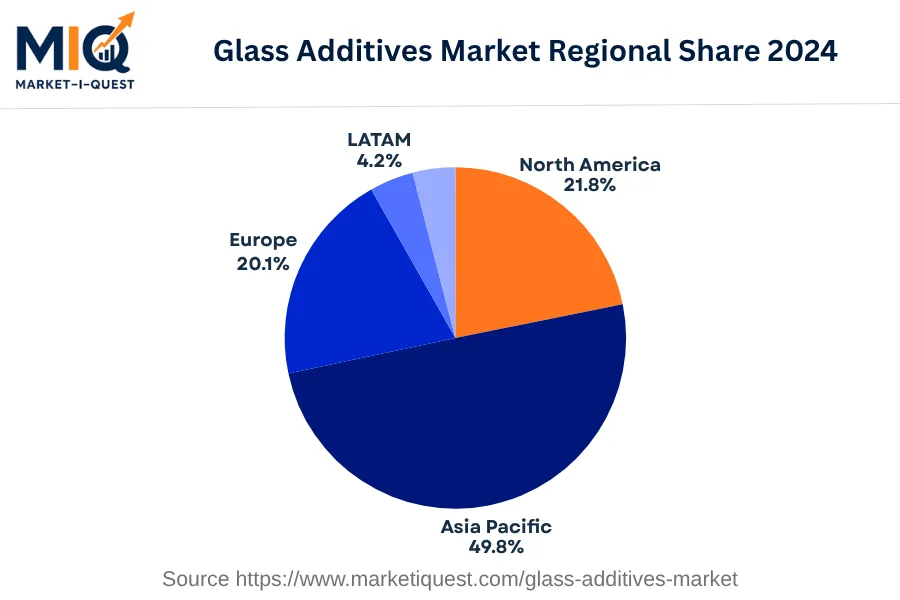

In 2024, the Asian Pacific market for glass additives experienced significant dynamics spurred by various factors. Drivers included increasing urbanization which amplified architectural glass demand particularly in China and India. Moreover, the growing consumer electronics industry led to escalated demand for high-quality display glass, primarily in Japan and South Korea. Regulatory pressures for efficient and environmental-friendly glass in the automotive and construction sectors across Australia and key ASEAN markets fueled market growth. Trends in this space included the shift towards nanotechnology in glass production, predominantly in China and India. Innovative partnerships, such as Japan-based AGC Inc.'s collaboration with Taiwanese company Industrial Technology Research Institute, further helped optimize processes.

Customer sentiments veered toward energy-saving glass, especially within the automotive and construction sectors across Australia, leading to a rise in the manufacture of low emissivity glass. In South Korea, the enforcement of stricter safety standards in the automotive sector compelled manufacturers to produce reinforced glass with additives. Lastly, expansion of e-commerce channels in key ASEAN markets significantly impacted the distribution and sales patterns of glass additives. Thus, the glass additives market in the Asia-Pacific region saw an uptick in 2024, driven by increasing demand, regulatory mandates, technological advancements, and changing market trends.