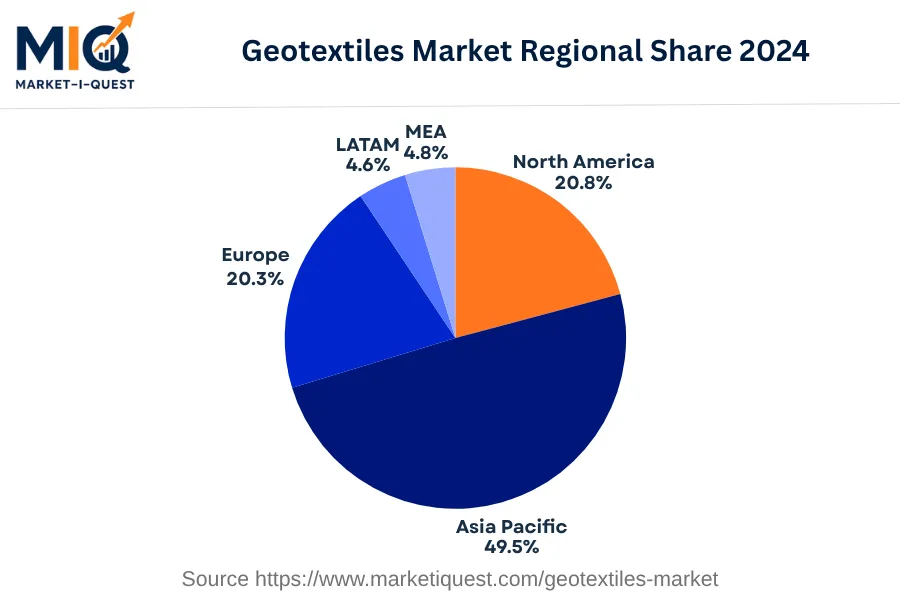

In 2024, the Geotextiles market in the Middle East and Africa showcased significant activity, propelled by diverse drivers and trends. Key drivers included stringent environmental regulations, particularly in Saudi Arabia and South Africa, which necessitated soil erosion control and waste management, thereby thriving geotextiles demand. Infrastructure development in countries such as the United Arab Emirates and Qatar saw governments prioritizing geotextiles adoption for ground stabilization and drainage systems. Technological advancements in non-woven geotextiles also gained momentum, enhancing their adoption in various sectors including oil and gas, utilities, and construction.

Trends observed in 2024 encompassed shifts in buyer behavior, particularly in Kenya and Nigeria, with increased preference for bio-based geotextiles due to their ecological and economic benefits. In terms of product shifts, woven geotextiles gained preference for their high load-bearing capacity, essential for the roads and railways developments witnessed in Egypt and Israel. Channel dynamics showcased a surge in online sales due to the influence of digital transformation. Regarding partnerships, a significant merger between leading textile manufacturers in Saudi Arabia and the UAE emphasized the strategic consolidation trend. The geotextiles market in the Middle East and Africa in 2024, therefore, exhibited growth, led by regulatory, infrastructural, and technological drivers, coupled with behavioral, product, channel, and strategic market trends.