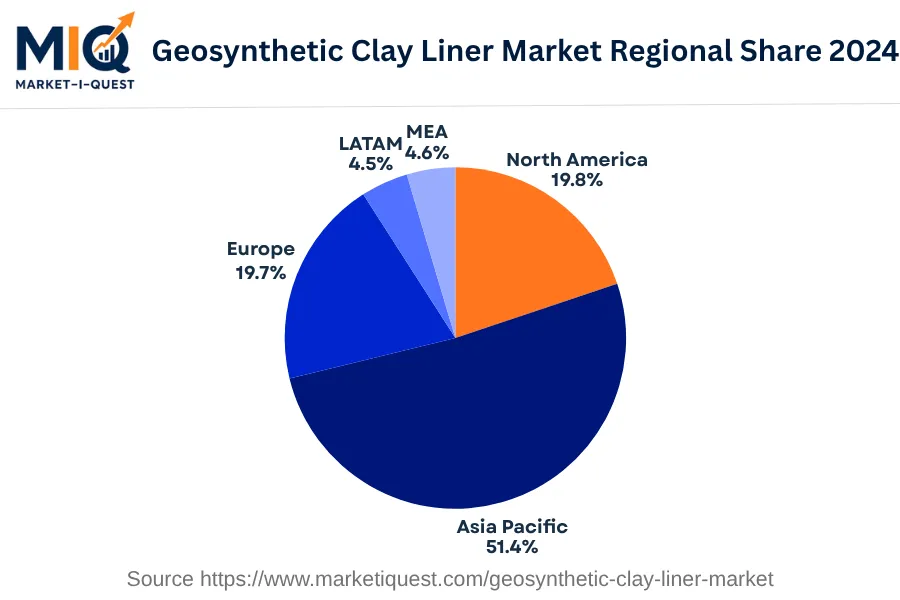

In 2024, the Geosynthetic Clay Liner market in Latin America was a growth driver in environmental management and waste containment projects. Increasing demand came as the region confronted escalating environmental concerns, as governments in Brazil, Mexico, Argentina, Colombia, Chile, and Peru implemented stricter regulations around industrial waste disposal and containment strategies. These policies, coupled with substantial investment in public and private infrastructures, necessitated the implementation of these liners to ensure effective and secure containment, thus driving market growth. Additionally, the trend toward adopting advanced and eco-friendly technology in waste containment practices influenced the sector's product dynamics. As a response to this demand, manufacturers focused on the innovation of cost-effective and environment-friendly liners. Moreover, partnerships and acquisitions within the market significantly increased with companies seeking to expand their geographical reach. The implementation of stringent waste management policies accelerated the technology shift in the market toward more effective products.

Major customers for these liners included utilities and manufacturing industries striving to meet set waste containment guidelines. The construction and mining sectors, particularly in countries like Brazil and Peru, also extensively used these liners due to the increase in environmental awareness and regulations within these sectors. Thus, the market in 2024 witnessed notable growth driven by increased regulation, investment, technology shifts, and the increasing environmental consciousness across different sectors.