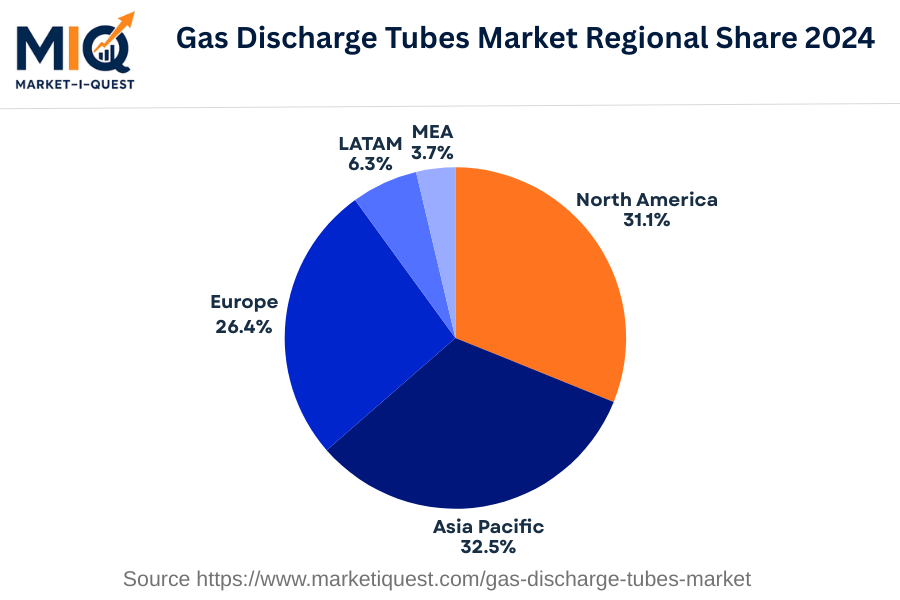

In 2024, the Gas Discharge Tubes (GDT) market in the Asia Pacific is characterized by a significant focus on enhancing electrical safety and surge protection across several sectors. The increasing adoption of renewable energy sources, particularly solar and wind, has driven demand for GDTs to protect sensitive electronics in power generation and distribution systems. Regulatory frameworks, such as China's "14th Five-Year Plan," emphasize improving electrical infrastructure, thereby fueling investment in surge protection devices. In India, government initiatives aimed at upgrading power quality standards further support GDT implementation in utilities and manufacturing.

Trends indicate a shift towards advanced materials in GDT manufacturing, enhancing performance and reliability. Buyers increasingly favor GDTs integrated into smart grid technologies, reflecting a broader move toward digitization in energy sectors across Japan and South Korea. Distribution channels are evolving, with greater emphasis on online platforms for strategic sourcing, driven by a skilled in tech customer base. Partnerships between manufacturers and utility providers are becoming common to co-develop tailored solutions. Stringent compliance with industry standards, especially in Australia’s electrical sector, is shaping purchasing decisions. Overall, the GDT market in Asia Pacific is characterized by its response to regulatory pressures and technological advancements, serving mainly to utilities, healthcare, and manufacturing sectors.