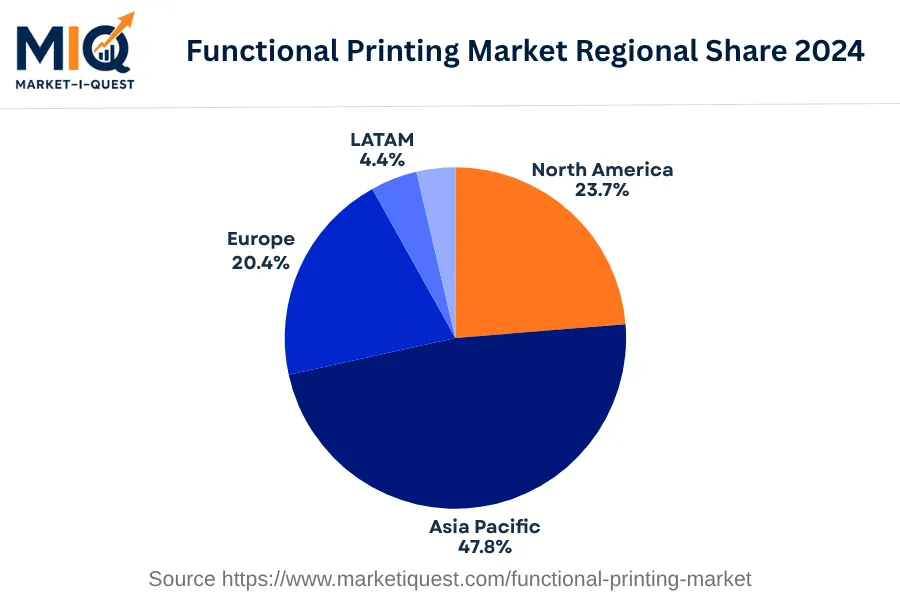

In 2024, the Functional Printing Market in Latin America presented an emerging ground of technological opportunity. Strong consumer electronics demand, fueled by the proliferation of IoT-enabled devices and growing disposable incomes in Brazil, Mexico, Argentina, Colombia, Chile, and Peru, encouraged manufacturers to innovate and diversify. Additionally, eco-conscious regulations amplified the adoption of green technologies like functional printing, allowing for energy-efficient manufacturing into different sectors such as healthcare, retail, and utilities.

Investment in research and development was evident, sparked by the strategic emphasis on advanced manufacturing technologies, fostering a conducive environment for market growth. Meanwhile, reductions in high-quality functional printing material costs contributed positively to the market's commercial feasibility.

Trends in 2024 included an increased integration of functional printing in packaging solutions throughout the retail sector and the adoption of cutting-edge technologies within the print supply chain, driven by smart manufacturing practices. Remarkably, the healthcare sector engaged in the market with applications in biosensors, medical packaging, and direct-to-patient communication tools. Partnerships and M&A activities marked the market landscape, allowing technology sharing and augmenting production capabilities. Finally, policy enforcement around electronic waste and sustainable production encouraged the drift toward eco-friendly functional printing, effectively shaping the market in Latin America in 2024.