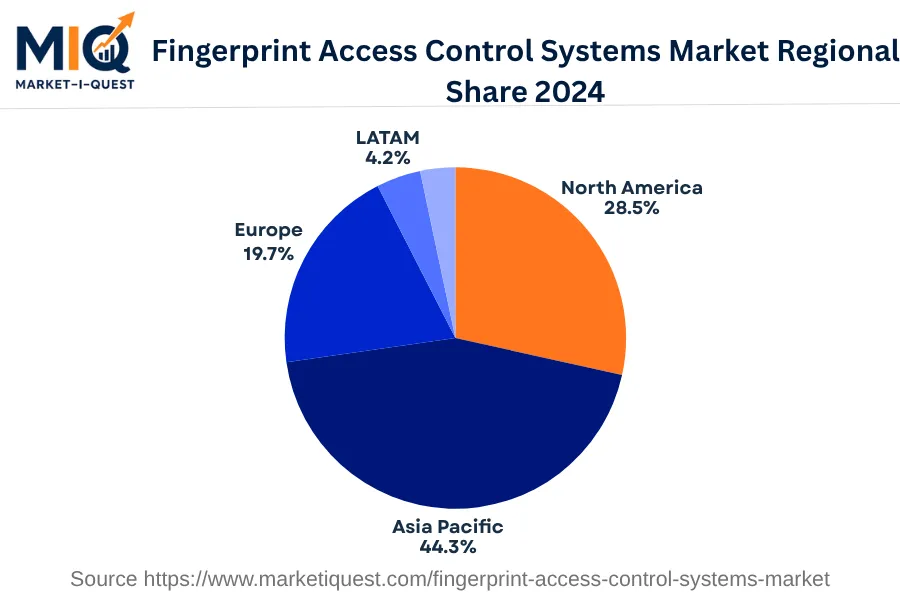

In 2024, the European Fingerprint Access Control Systems market saw significant development owing to various factors and trends. The prevalent drivers include increased digitization of businesses across sectors such as enterprise, healthcare, utilities, and retail. The adoption of robust, biometric security measures due to privacy regulations like General Data Protection Regulation (GDPR) and the vast governmental investments in public security infrastructures, particularly in countries like Germany, the UK, and France improved demand. Notably, technological advancements and more cost-effective solutions also led to an upsurge in market expansion.

Among the observed trends, enhanced buyer preference towards security systems with user-friendly interfaces and seamless integration surfaces as vital. There's a distinct shift towards cloud-based access control systems due to their flexibility and scalability. The prominent tech shift is evident in innovations, such as sophisticated multi-modal systems, which offer higher identification accuracy. Notably, Italy and Spain, with their fast-growing tech start-up scenes, have been witnessing a surge in strategic partnerships and mergers, favouring the expansion and diversification of product offerings. Policy enforcement, such as the UK's Biometric Data Protection Act, is being enacted to regulate and ensure the responsible use of biometric tech, contributing to the market's maturity and long-term sustainability.