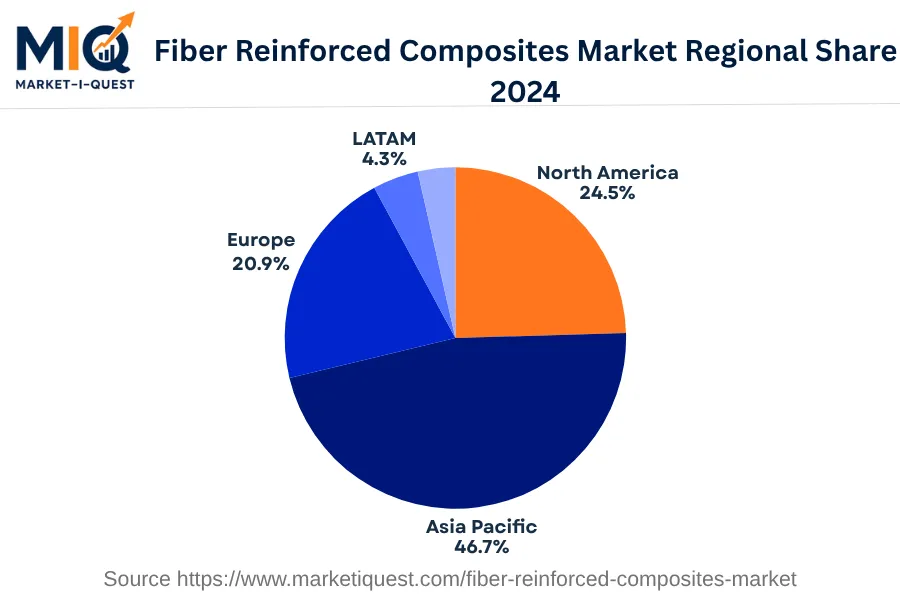

In 2024, the Fiber Reinforced Composites Market in the Asia Pacific underwent dynamic growth driven by various significant factors. Rising demand from key sectors such as automotive, aerospace, and construction, more prominently from China and India, acted as the primary stimulant. Enhanced adoption of technology and innovative product development, especially in Japan and South Korea, bolstered the market further. Additionally, government policies favoring manufacturing practices, like Made in China 2025, have led to amplified investments in the composites sector.

Conversely, shifting buyer behaviors revealed a clear interest in lightweight and high-performance materials, augmenting the market's dynamism. The automotive sector, seeking fuel efficiency, and the construction industry, with its increasing demand for corrosion-free materials, particularly promoted this trend. Notably, partnerships and M&As among material producers and end-user industries strengthened the collaborative framework in the composite market. A significant shift emerged in channel dynamics, with a steadily was growing digital presence. Meanwhile, in response to environmental concerns, the enforcement of sustainability standards encouraged the use of eco-friendly materials, particularly in Australia and key ASEAN markets. Consequently, the fiber reinforced composites sector was considerably influenced by these ongoing drivers and trends in 2024.