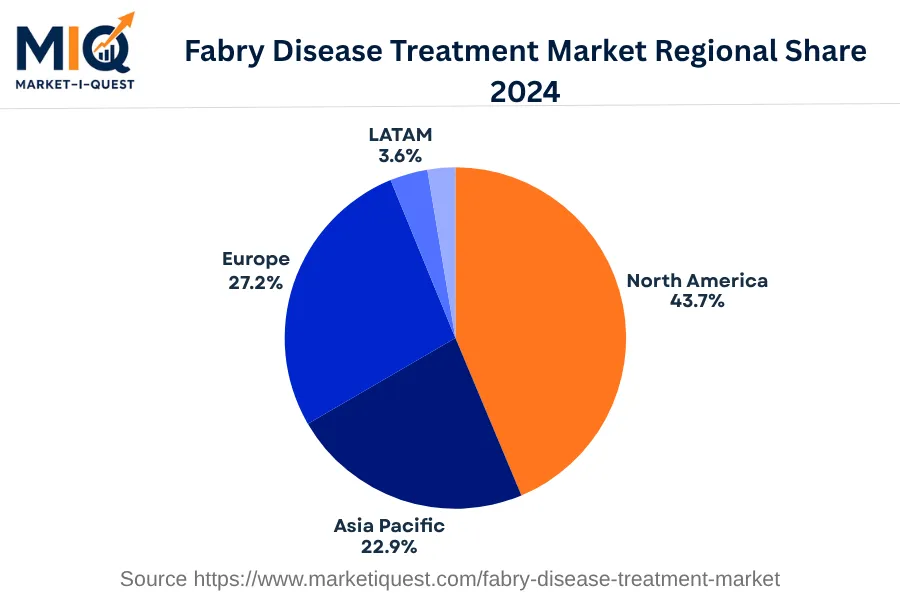

In 2024, the Fabry Disease Treatment Market in Europe was in a strong position due to various factors that drove demand and significant trends. Regulatory acceptance, increased investment, innovative technology adoption, and the amendments in disease treatment protocols in countries such as Germany, the United Kingdom, France, Italy, Spain, the Nordics, Benelux, and Central & Eastern Europe shaped the market dynamics. Advanced treatment procedures, reduced prices of enzyme replacement therapies, and the availability of genetic diagnostic tools stimulated market growth.

Increased awareness and diagnosis rates among healthcare providers and patients positively influenced the demand. Private sector entities, government bodies, and NGOs endeavored to enhance patient access to enzyme replacement therapies, consequently boosting the market.

Definite trends also prevailed in the Fabry Disease Treatment Market. A conspicuous shift towards personalised treatment options and gene therapies evidenced the evolving therapeutic landscape. The emergence of strategic alliances and partnerships among key players aimed to expedite drug development and leverage product portfolios. Policymakers enforced stringent regulations ensuring the safety and efficiency of novel therapies. The sectors majorly involved consisted of healthcare providers, genetic research institutions, pharmaceutical manufacturing industry, government health agencies, and hospital chains. Therefore, in 2024, the Fabry Disease Treatment Market in Europe was defined by a combination of driving factors and fundamental shifts in treatment procedures, regulatory landscape, and partnership models.