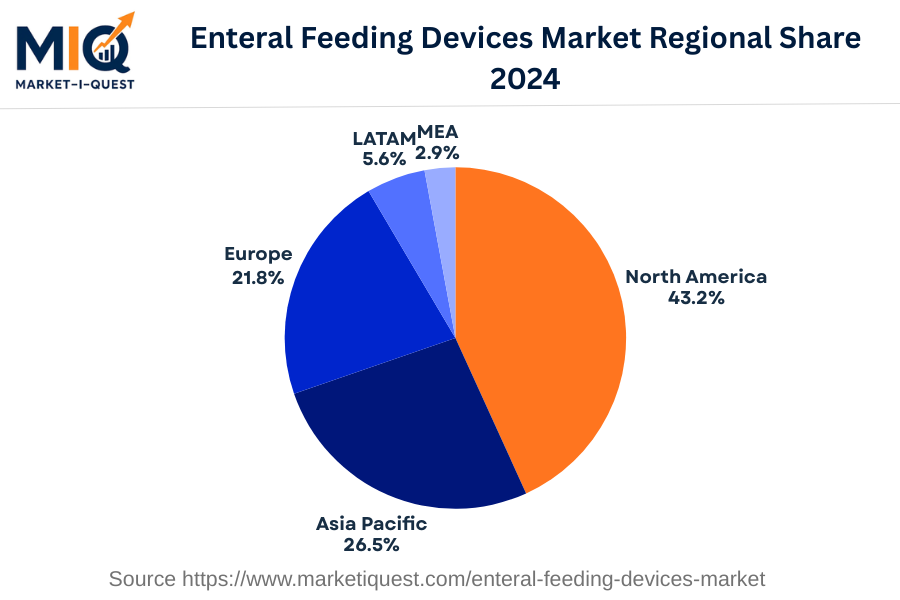

The enteral feeding devices market in Europe in 2024 is characterized by growing demand driven by an increasing prevalence of chronic diseases, necessitating nutritional support for patients with conditions such as stroke and cancer. Regulatory frameworks across the region, particularly the European Medical Device Regulation (EU MDR), have heightened safety standards, compelling manufacturers to invest in compliance and quality improvements. This regulatory shift, coupled with technological advancements in feeding pumps and accessories, has fostered an environment beneficial to innovation and investment in enteral feeding solutions.

Buyer behavior is increasingly leaning towards home care, as healthcare providers and patients seek to optimize care settings, pushing a shift toward portable and user-friendly devices. Additionally, there is rising interest in integrated systems that combine nutrition management with digital health technologies, enhancing patient monitoring and outcomes. Collaborative efforts and mergers and acquisitions among key players, such as Nutricia and Abbott, signify a trend towards enhancing portfolio offerings and expanding market reach. Furthermore, reimbursement policies across Germany, France, and the UK are evolving to support enteral feeding, creating favorable conditions for market growth. Overall, the dynamic landscape is marked by technological shifts, regulatory compliance, and evolving care models.