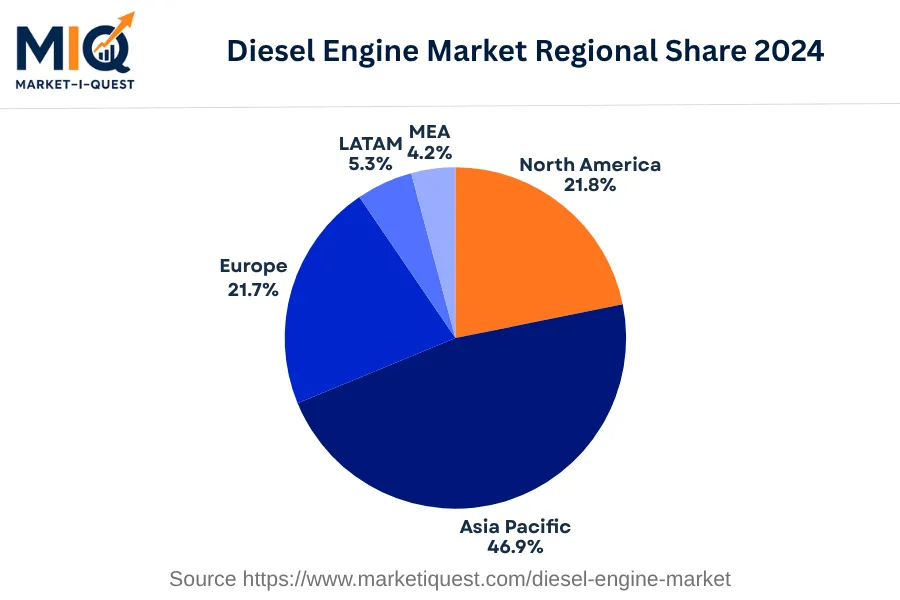

In 2024, the Diesel Engine Market in Latin America demonstrated significant growth fueled by various factors. Increased demand, driven by the flourishing commercial vehicle sector, primarily in Brazil, Mexico, and Argentina, put direct pressure on production and subsequently on prices. Stringent emission standards imposed by governments, particularly in Chile and Colombia, stimulated the adoption of cutting-edge diesel engine technology. Additionally, heavy investments made in the manufacturing and mining sectors across Peru and Mexico kick-started the supply dynamics.

Consumer behavior, influenced by the adherence to environmental norms and regulations, trended towards more technologically advanced and fuel-efficient diesel engines. The shift towards products that complied with emission standards was evident across sectors like utilities, manufacturing, and retail. Larger enterprises in the region were found showing an increased preference for Original Equipment Manufacturer (OEM) partnerships, leading to a boom in M&A activity, particularly in the Brazilian and Mexican markets. Another significant trend was the enforcement of Euro VI and Proconve P8 emission standards across several Latin American countries, which had a direct effect on product designs and buyer preferences. Lastly, a drift towards online sales channels, redefining the way manufacturers, distributors, and customers interacted, was observed, indicative of the region's changing retail dynamics.