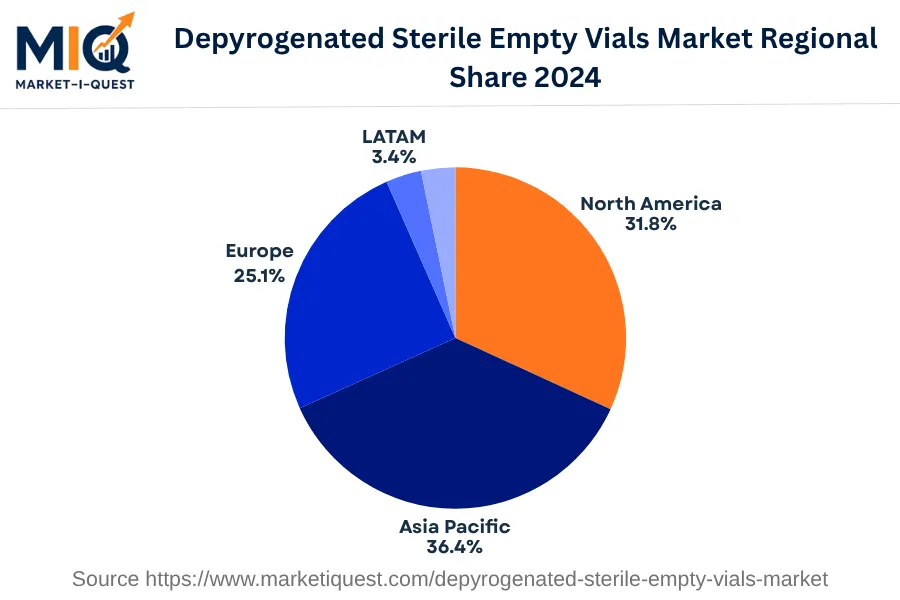

In the base year 2024, the Depyrogenated Sterile Empty Vials Market experienced substantial growth in Latin America due to robust healthcare sector advancements and strict regulatory compliance. Significant investments in the pharmaceutical sector, primarily in countries like Brazil, Argentina, and Mexico, drove demand for sterile vials, instigating market expansion. Regulatory bodies imposed stringent policies ensuring safe and effective drug delivery, pushing manufacturers to adopt advanced technologies for sterility. Surging export of drugs from Latin America, especially Brazil and Mexico, influenced supply dynamics noticeably, periodically affecting pricing structures of vials.

Regarding trends, buyer behavior shifted towards demand for high-quality, reliable sterile empty vials, influenced by escalating health safety concerns. Technological advancements emerged in vial manufacturing processes, employing heat-treatment methods for depyrogenation, gaining traction especially in advanced healthcare markets like Argentina and Chile. Distribution channels underwent reorganization with pharmaceutical companies forming strategic alliances and M&A with vial manufacturers to ensure a steady supply of depyrogenated sterile vials. Increased scrutiny led to strict policy enforcement on sterile procedures, transforming the market landscape predominantly in Peru and Colombia. The primary customer base encompassed the pharmaceutical industry and healthcare institutions across Latin America, with high demand generated from sectors with an emphasis on injectable drug production.