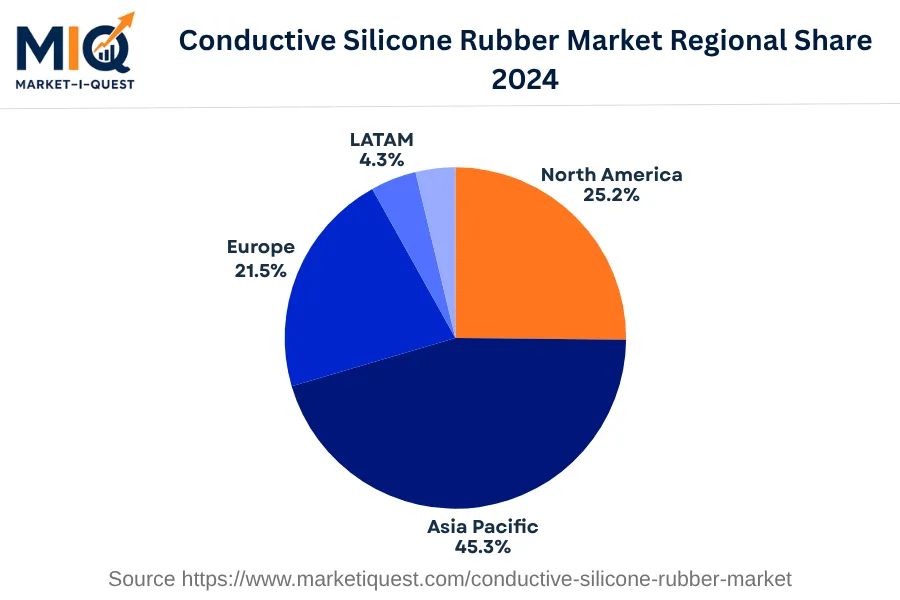

In 2024, the Conductive Silicone Rubber Market in Europe showed a notable level of demand, specifically in Germany, the United Kingdom, France, Italy, Spain, the Nordics, Benelux, and Central & Eastern Europe. Heightened investment in the automotive and electronics industries was a significant driver of this demand, as improvements in technology necessitated the use of conductive silicone rubber in integral components. Additionally, new regulatory requirements regarding safety standards in these sectors encouraged further adoption of this material.

Simultaneously, an evident shift in buyer preference towards products featuring this material, particularly in the automotive sector, was recorded. Advancements in manufacturing technology also enabled easier production and application of conductive silicone rubber, thus making it more attractive to industries such as healthcare, utilities, and manufacturing. There was an increase in partnerships and M&A activities amongst key players within the market, primarily aimed at expanding product offerings and consolidating market position. The UK government’s enforcement of strict safety and efficiency standards in the electronics and automotive sectors also contributed to an increased demand for conductive silicone rubber. Customers from a broad range of sectors, including enterprise, government, healthcare, utilities, manufacturing and retail, showed increased interest in adopting technologies and products featuring conductive silicone rubber, further bolstering its market presence in 2024.