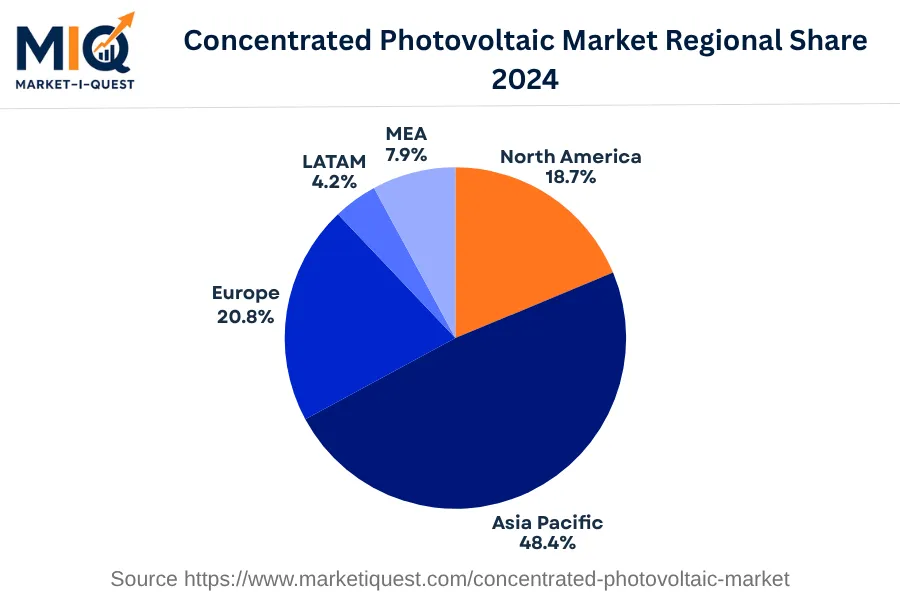

In 2024, the Asia Pacific Concentrated Photovoltaic (CPV) Market experienced intensified demand due to increased government initiative and renewable energy policies. China's commitment to renewable energy, epitomized by its 13th Five-Year Plan, and India's National Solar Mission, catalyzed a surge in demand for CPV technology. Investments from multinational corporations such as IBM and SunPower further enriched the market stability. Technological advancements, particularly in High Concentration Photovoltaic (HCPV) systems, promoted adoption throughout the region, especially in Japan and South Korea.

Simultaneously, falling solar module prices challenged the profitability of CPV manufacturers but incentivized end-users, primarily utilities and manufacturing sectors. Increasing industrialization in key ASEAN markets led to a trend for private company-led CPV projects, shifting away from the government-led model. Strategic partnerships, such as those between Suncore and China Huadian Corporation, impacted market dynamics, consolidating market leadership. Regulatory enforcement, particularly in Australia, shaped the CPV market through measures to enhance grid connectivity and renewable purchase obligations. The retail market saw a growing interest in CPV, driven by increasing environmental consciousness and the shifting focus towards emission reduction. In contrast, the enterprise sector remained slow in technology adoption, mostly due to high setup costs. Nevertheless, the continuous development and promotion of CPV systems contributed to robust market health in the region during 2024.