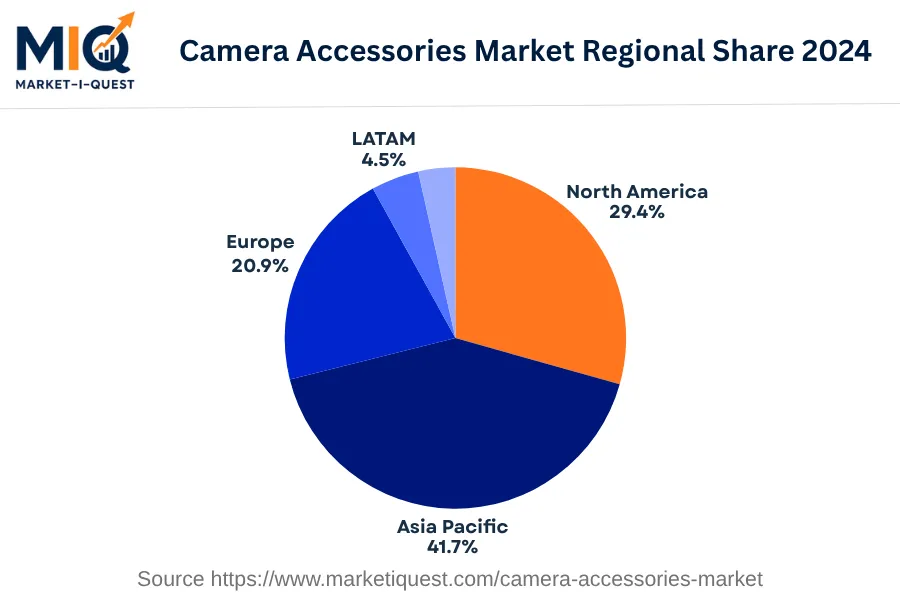

In 2024, the Camera Accessories Market in the Asia Pacific showcased significant dynamism, marked by an uptick in consumer preference for superior photography equipment. Key demand drivers included the escalating popularity of digital photography in China and India, spurred by the rise in social media usage and growing urban middle-class population. Additionally, progressive trade policies bolstered the import of superior quality camera accessories in Australia, Japan, and key ASEAN markets. Innovative technology adoption, such as drone photography in South Korea, generated fresh demand.

Shifting trends included an increased inclination towards online shopping for camera accessories, as evidenced in the digital marketplaces of China and India. The rise in partnerships between camera accessory manufacturers and e-commerce platforms further contributed to this trend. In Japan, demand for mirrorless cameras boomed, signaling a shift in product preference. Meanwhile, Australia witnessed a surge in environmental photography, leading to greater demand for specialized camera accessories. Standardization policies implemented across several markets, like ISO standard in camera lenses, maintained the market's competitiveness.

Significant customer segments included industries such as entertainment, media, tourism, and e-commerce. Retail consumers, like photography enthusiasts and social media influencers, formed an equally significant customer base. Furthermore, governmental sectors across the Asia Pacific harnessed high-end camera accessories for surveillance and security applications, thereby stimulating the market.