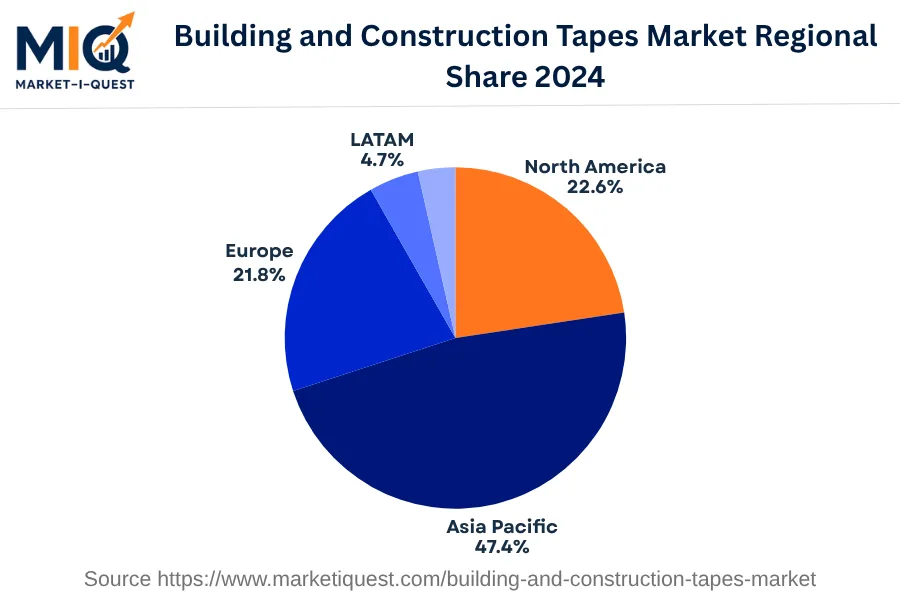

In 2024, the Building and Construction Tapes Market in North America experienced noticeable growth. Driving forces behind this momentum included demand for advanced adhesive solutions across various construction activities, substantial investments in residential and commercial real estate, especially in the U.S. and Canada, and innovative technology adoption. Regulatory policies, such as the U.S.'s Federal Green Construction Code, promoted the use of environment-friendly adhesives, while competitive pricing strategies influenced supply dynamics.

Several trends in 2024 shaped the Building and Construction Tapes Market. Increased buyer preference for durable, resilient, and easy-to-use adhesives revamped product offerings, favoring tapes with advanced capabilities. Digital channels played a significant role in product promotion and distribution, enhancing market reach. Strategic partnerships and mergers and acquisitions were rampant, particularly among manufacturers aiming to expand their market presence. In line with evolving construction standards, policy enforcement for sustainable building practices intensified, creating an upward demand curve for green adhesives. Various sectors, such as enterprise, government, manufacturing, and utilities, significantly adopted building and construction tapes. From repairing minor wear and tear in office spaces to large-scale public infrastructural projects, the role of construction tapes was ubiquitous, making them an indispensable part of North American construction in 2024.