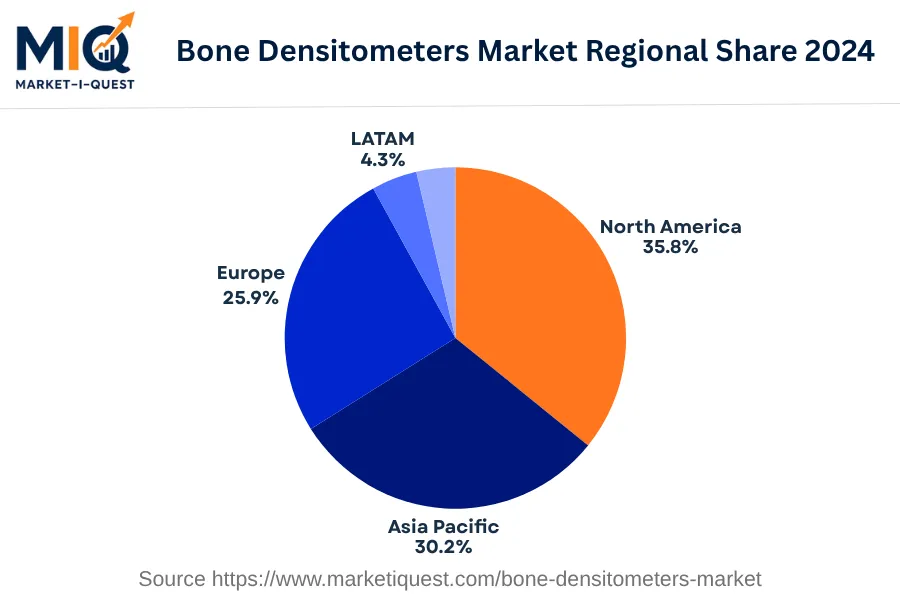

In 2024, the European Bone Densitometers Market experienced substantial growth, dominated by key players in Germany, the UK, France, Italy, Spain, the Nordics, Benelux, and Central & Eastern Europe. Main growth drivers included heightened awareness of osteoporosis prevention, increased healthcare investment in bone health diagnostics, and accelerated technology adoption in healthcare institutions. Regulatory bodies promoted osteoporosis screening for post-menopausal women, urging earlier and more frequent usage of bone densitometers. Noteworthy was the surging demand in Central & Eastern Europe due to a notable rise in geriatric population requiring bone health services.

In terms of trends, patient preference for non-invasive procedures amplified the popularity of Dual-energy X-ray Absorptiometry (DXA) densitometers. The healthcare sector embraced digital platforms for image analysis, rendering examinations more accurate and efficient. Increased collaborations, such as the notable partnership between GE Healthcare and Quibim, allowed seamless integration of advanced analytics into bone health services. Following EUnetHTA's guidelines, densitometer standards were consistently enforced, leading to quality assurance and improved patient safety. Primary customer sectors included hospitals and diagnostic centres, followed closely by academia and research institutions. A meaningful proportion of sales originated from government procurement, driven by national healthcare programs promoting bone health. Overall, the European market for bone densitometers in 2024 showed significant potential for segmentation, customization, and technological advancement.