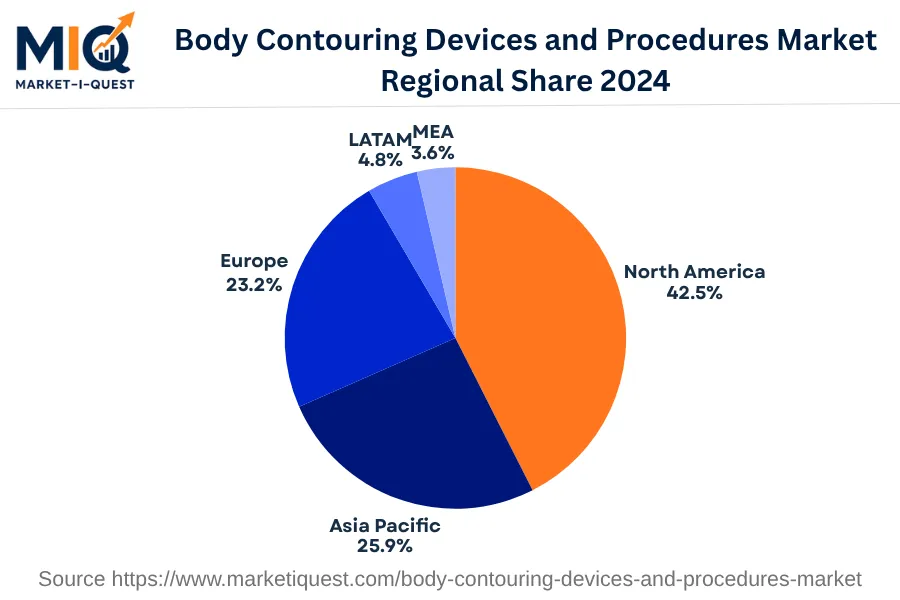

In 2024, the Body Contouring Devices and Procedures Market experienced significant incremental growth throughout the Middle East and Africa, predominantly within Saudi Arabia, UAE, South Africa, Nigeria, Kenya, and Israel. Critical demand drivers included a rising middle class, increasingly health and beauty-conscious consumers, and advancements in non-invasive cosmetic procedures. Emerging technologies and the introduction of sophisticated devices escalated the market activity across these regions. The increasing investments from healthcare institutions, along with supportive government policies for medical device importation and use, particularly in Israel and South Africa, stimulated the market acceleration.

In terms of trends, non-surgical treatments like radiofrequency and high-intensity focused ultrasound were prevalent, spearheaded by the growing preference for less invasive methods with minimal recovery time. Additionally, the uptick in medical tourism, notably in UAE and Saudi Arabia, attracted a global customer base seeking superior cosmetic services at competitive pricing. Lastly, strategic collaborations and partnerships between regional hospitals and global device manufacturers were witnessed, aiding technology transfer and enhancing healthcare service standards in cosmetic treatment. This market movement primarily catered sectors like healthcare and hospitality which included government-driven health institutions, private boutique health clinics, and luxury hotels offering wellness services. As the regional population's beauty aspirations grow, so does the Body Contouring Devices and Procedures Market.