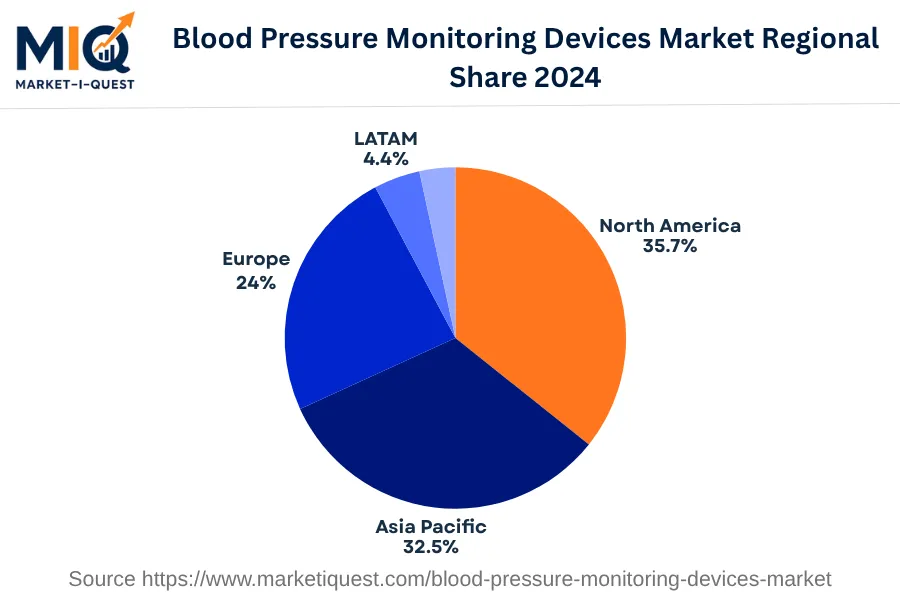

In 2024, the Blood Pressure Monitoring Devices Market in Latin America showed dynamic growth due to several drivers and trends. Primary growth drivers included increased healthcare investment in countries like Brazil and Argentina, advanced adoption of digital health technologies in Mexico and Chile, and heightened awareness of hypertension risks in Colombia and Peru. New regulation standards across LATAM, aiming for better diagnosis quality, prompted manufacturers to develop precise, user-friendly devices. Robust demand was further catalyzed by rising telemedicine practices in metropolitan areas, where home blood pressure monitoring became a standard.

Trends observed in 2024 revealed a shift towards ambulatory and wearable monitoring devices, primarily adopted by younger, tech-savvy customers. The rapid growth of e-pharmacies and online healthcare platforms facilitated easy access to these devices for consumers. Partnerships among device manufacturers and health-tech firms flourished, enhancing product development and distribution channels. Brazil and Mexico, leading in digital health infrastructure, prominently drove this trend. The LATAM region also saw strict policy enforcement pertaining to product standards and patient safety, shaping manufacturers' strategies. Key clientele included healthcare facilities, government health programs, and the growing home healthcare sector. In summary, the LATAM Blood Pressure Monitoring Devices Market in 2024 was significantly influenced by healthcare investment, technology adoption, regulatory standards, and digital channel dynamics.