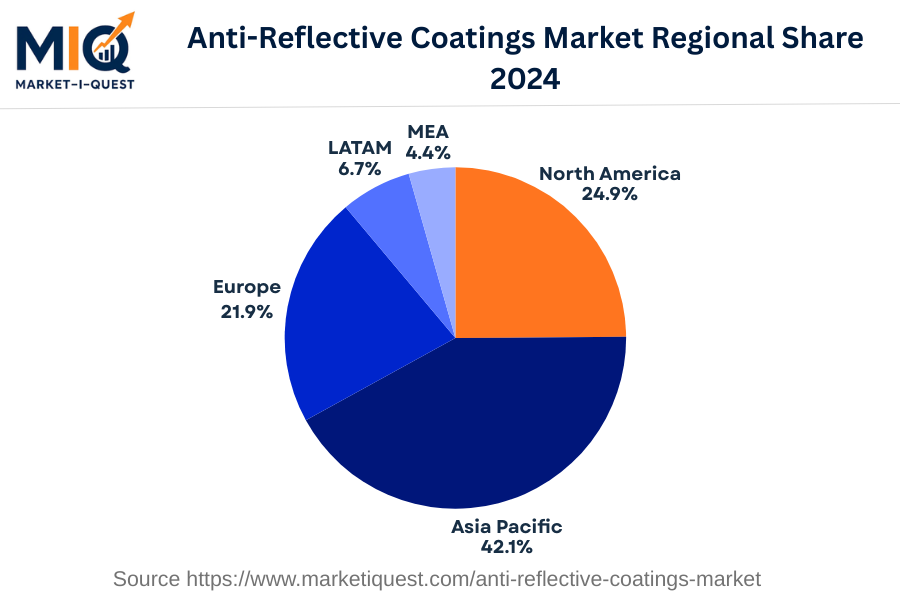

The Anti-Reflective Coatings Market share in North America in 2024 is driven by increasing demand across various sectors, particularly in electronics, automotive, and healthcare. The proliferation of smartphones and other electronic devices fuels the need for high-performance anti-reflective coatings, reducing glare and improving visibility. Regulatory standards, such as those set by the U.S. Environmental Protection Agency (EPA), promote the adoption of coatings that enhance energy efficiency and safety in automotive applications. Additionally, investments in innovative coating technologies, including nano-coatings, are reshaping product offerings, making them more durable and effective.

Trends indicate a shift in buyer behavior toward multi-functional coatings that offer enhanced qualities such as scratch resistance alongside anti-reflective properties. E-commerce platforms are becoming increasingly important channels for distributing these coatings, allowing manufacturers to reach a wider audience directly. Furthermore, partnerships between coating manufacturers and tech companies are emerging to develop customized solutions for specific applications, particularly in the optics sector. Policymaking, especially related to sustainability and environmental impact, influences manufacturing standards, compelling companies to innovate and comply with new regulations. These dynamics reflect a mature and evolving market landscape within the region.