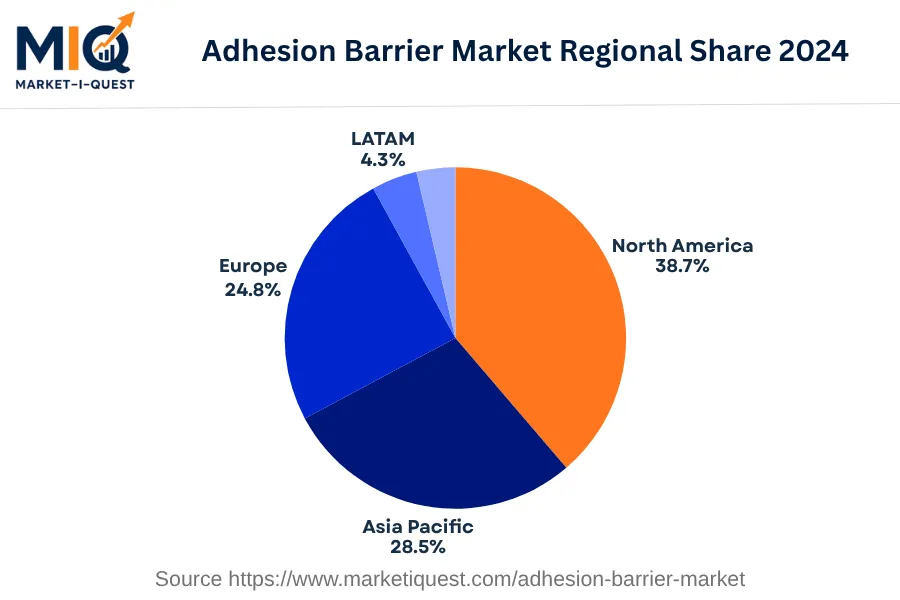

In 2024, Europe's adhesion barrier market remained strongly rooted in the dynamic healthcare sector. The market's growth was driven primarily by the rising frequency of surgeries, resultant adhesion complications, and the need for effective adhesion prevention measures. The increased funding in healthcare research & development (R&D) and technological advancements, especially in Germany, the United Kingdom, France, and Italy, also propelled the market. Further, the cost-efficacy of adhesion barriers, particularly in Central & Eastern Europe, and the Benelux region, stimulated demand as healthcare providers sought to minimize postoperative complications.

Parallel to these drivers, several market trends were emerging. The Nordic countries, for instance, showcased a notable inclination toward synthetic adhesion barriers due to their high effectiveness and safety. Product innovations were significant, with France and Italy leading in the development of advanced, bioresorbable adhesion barriers. Channel dynamics shifted, too, as digital platforms provided wider access to these products, particularly in Spain. Furthermore, Germany witnessed several strategic partnerships and mergers and acquisitions (M&As) among prominent healthcare companies aiming to expand their reach in the adhesion barrier market. Lastly, stringent policy enforcement, particularly in the United Kingdom, prompted the market to adhere to high-quality standards, impacting product development. Hence, the European adhesion barrier market in 2024, was a blend of demanding health conditions, innovative technologies, reshaped channels, and strict policies.