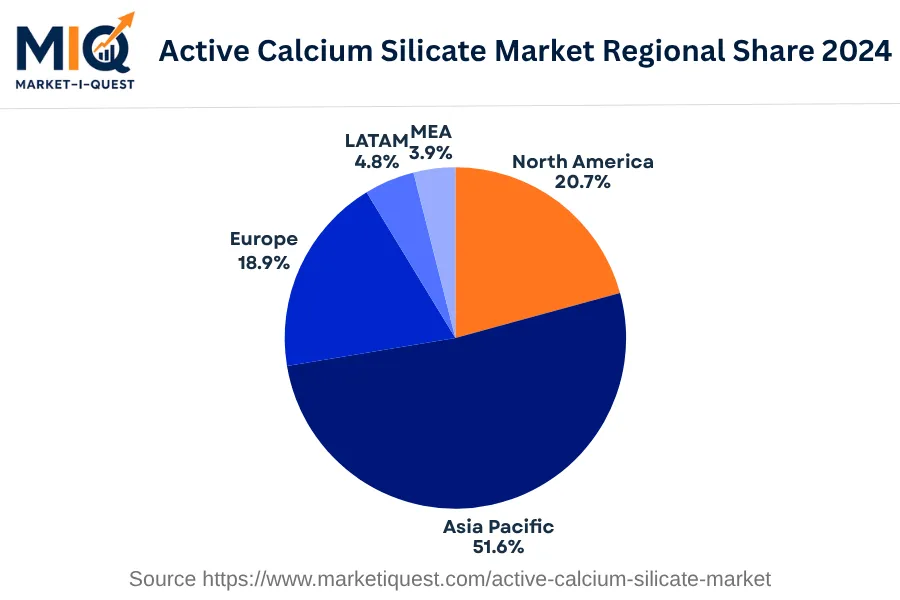

In 2024, the Active Calcium Silicate market in Latin America (LATAM) demonstrated a heightened demand driven primarily by construction, ceramics, and fire protection industries. An inflow of foreign investments, particularly in Brazil and Mexico's infrastructure development, created robust demand. In Argentina and Chile, stricter enforcement of fire safety norms compelled construction and manufacturing sectors to incorporate fire-resistant materials like Active Calcium Silicate. Technological adoption in Colombia and Peru's ceramics industry further propelled the market, with Active Calcium Silicate being favored for its thermal insulation properties.

Market trends predominantly revolve around ecological considerations and stringent regulatory compliance. In Brazil, Chile, and Argentina, end-users increasingly prefer Active Calcium Silicate for its non-toxic and bio-degradable attributes, aligning with their sustainability goals. LATAM's ongoing digitalization wave, particularly in Mexico and Peru, led to partnerships between local manufacturers and tech firms to develop advanced manufacturing processes, thereby optimizing supply. Compliance with the ‘Reglamento Técnico Centroamericano’ emerged as a notable trend, as companies navigated the regulatory landscape. The retail and e-commerce channels further witnessed accelerated sales due to the ease of product comparison and consumer awareness. The LATAM Active Calcium Silicate market, in 2024, was fueled by a blend of investment, regulatory compulsions, technological advances, and changes in consumer behavior.